Quarterly Economic and Market Review

- Geopolitical Risks Ease — A fragile cease-fire in Iran reopened the Strait of Hormuz, easing energy supply concerns and helping markets recover from volatility.

- Policy Expectations Shift — Higher inflation and a new Federal Reserve Chairman pushed markets away from expecting interest rate cuts and toward a higher-for-longer rate environment.

- Market Leadership Broadens – Continued enthusiasm for AI helped lift equity markets to new highs, with leadership expanding beyond the Magnificent Seven into a wider range of sectors and company size.

From conflict to negotiations

Throughout the second quarter, markets remained focused on the conflict in Iran and the uncertainty surrounding global energy supplies. With the Strait of Hormuz closed to commercial shipping, a significant share of the world's oil, natural gas, and fertilizer exports were temporarily disrupted. Energy markets reacted quickly, with crude oil rising above $115 per barrel in April and gasoline prices following. Investors feared that a prolonged closure could push energy prices substantially higher and potentially trigger a global recession.

Conditions improved as the quarter progressed. On June 17, all parties signed the Islamabad Memorandum of Understanding establishing a cease-fire, reopening the Strait of Hormuz and creating a framework for formal negotiations. The financial markets responded favorably. Global equities recovered, while crude oil prices declined to approximately $70 per barrel by quarter-end.

Although much of June's economic data has yet to be released, the global economy appears to have weathered the disruption better than initially expected. Positive GDP growth is still anticipated across most major economies, S&P 500 earnings are projected to grow approximately 24% in 2026 and the U.S. labor market has been fairly stable with a 4.2% unemployment rate. Even so, renewed hostilities remain a meaningful risk. Any disruption to global energy supplies could quickly reignite inflationary pressures and place upward pressure on interest rates.

Inflation and interest rates – a revised outlook

The second quarter significantly altered expectations for monetary policy. Higher energy prices pushed inflation modestly higher, a new Federal Reserve Chairman took office and the labor market remains stagnant — prompting investors to reassess the path of interest rates.

While inflation remains well below the levels reached in 2022, recent trends have moved in the wrong direction. Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) inflation both increased to roughly 4.2% year-over-year, remaining well above the Federal Reserve's 2% target. At the same time, longer-term inflation expectations have remained relatively stable, suggesting investors continue to view the recent increase as manageable rather than permanent.

Kevin Warsh assumed the role of Federal Reserve Chairman on May 22. Although previously viewed as supportive of lower interest rates, the recent inflation backdrop has prompted more hawkish commentary. Markets have largely shifted away from expecting rate cuts this year. The expectation now is for one or two 0.25% increases to the Fed’s policy rate by the end of 2026.

This shift has extended beyond the United States. The European Central Bank raised interest rates by 0.25% in June, while the Bank of Japan continued tightening monetary policy after ending its long period of negative interest rates. Together, these moves suggest a broader transition toward more restrictive global monetary policy.

Capital markets – looking beyond the headlines

Despite continued uncertainty surrounding the conflict in Iran, financial markets increasingly looked beyond the immediate geopolitical risks. The S&P 500 and NASDAQ reached new record highs during June, while the Dow Jones Industrial Average climbed above 52,000 for the first time.

Technology companies tied to artificial intelligence quickly resumed market leadership following the initial peace negotiations, supported not only by improving geopolitical sentiment but also by strong corporate earnings, continued capital investment and resilient economic growth. As investor confidence improved, market gains broadened beyond large technology companies, benefiting a wider range of sectors and company sizes.

Fixed income markets reflected the changing interest rate outlook. Treasury yields moved higher throughout much of the quarter, with the 10-year Treasury briefly reaching 4.66% in May before easing as tensions in the Middle East subsided. Please see reverse side for important disclosure information. Private markets were less resilient. Several private credit funds experienced elevated redemption requests, highlighting the liquidity challenges that can accompany less-liquid investments. As Treasury yields increased, many investors reassessed the tradeoff between higher liquidity and the incremental return offered by private credit strategies.

Mega IPOs

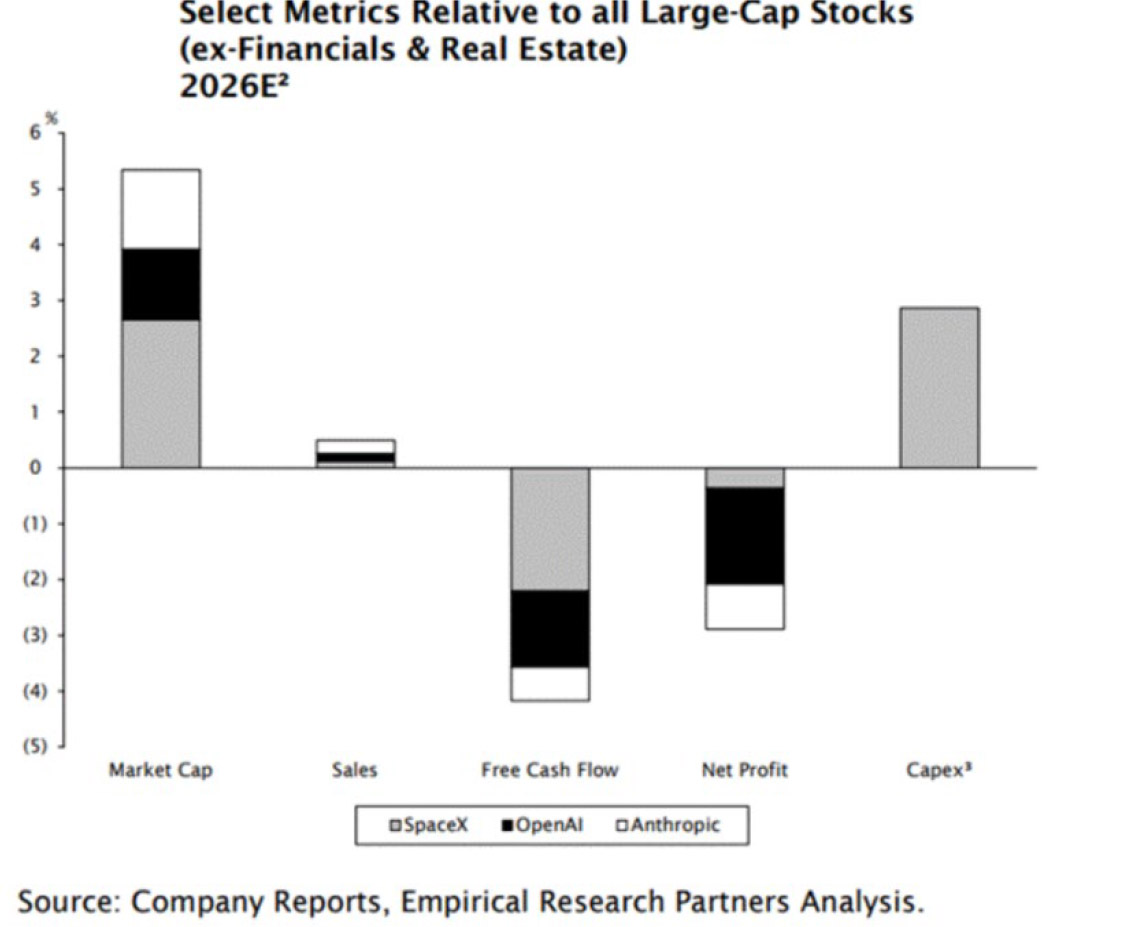

SpaceX became the latest example in June, reaching a valuation of approximately $1.7 trillion following its initial public offering. Despite reporting nearly $19 billion in revenue during 2025, the company lost roughly $5 billion for the year. Anthropic and OpenAI are expected to follow with similar historic public offerings later this year, despite neither company currently being profitable. These valuations reflect more than optimism surrounding individual businesses—they signal investors' belief that artificial intelligence will become one of the defining technologies of the next decade.

Unlike the previous generation of high-growth software companies, today's AI leaders require extraordinary amounts of capital. Developing frontier AI models demands massive investments in data centers, specialized chips, electrical infrastructure and computing capacity. Rather than scaling with relatively modest capital requirements, AI companies are investing billions of dollars each quarter simply to remain competitive. Much of this spending has been financed by private investors and the cash flows of the largest technology firms, but as capital needs continue to grow, the industry will increasingly rely on public equity markets, debt financing, or a meaningful acceleration in revenues.

Artificial intelligence remains in its early stages and the investment required to build its infrastructure increasingly resembles the construction of railroads or telecommunications networks more than the software boom of the last two decades. While these companies may offer compelling long-term opportunities, they also require investors to make significant assumptions about future growth and profitability. Maintaining a disciplined investment process may occasionally mean passing on the market's most attention-grabbing opportunities, but it has historically been the foundation for producing consistent, repeatable investment results.

Sources:

Mag 7 Chart

https://www.businessinsider.com/stock-market-charts-rotation-stocks-tech-value-investing-strategy2026-6

“Expect IPO Value…” Chart

https://www.howardlindzon.com/p/momentum-monday-dot-com-2-0-the-ai-edition-spacex-anthropicand-open-ai-ipo-or-death

“Select Metrics Relative…” Chart

Empirical Research Portfolio Strategy June 2026

Investment, Securities and Insurance Products:

NOT

FDIC INSUREDNOT BANK

GUARANTEEDMAY

LOSE VALUENOT INSURED BY ANY

FEDERAL AGENCYNOT A

DEPOSITAssociated Bank and Associated Bank Private Wealth are marketing names Associated Banc-Corp (AB-C) uses for products and services offered by its affiliates. Securities and investment advisory services are offered by Associated Investment Services, Inc. (AIS), member FINRA/SIPC; insurance products are offered by licensed agents of AIS; deposit and loan products and services are offered through Associated Bank, N.A. (ABNA); investment management, fiduciary, administrative and planning services are offered through Associated Trust Company, N.A. (ATC); and Kellogg Asset Management, LLC® (KAM) provides investment management services to AB-C affiliates. AIS, ABNA, ATC, and KAM are all direct or indirect, wholly-owned subsidiaries of AB-C. AB-C and its affiliates do not provide tax, legal or accounting advice. Please consult with your advisors regarding your individual situation. (1024)

Readers should not consider this update of the economic and investment environment as analysis upon which to make investment decisions or recommendations of strategies or particular securities. Past performance is no guarantee of future results. (1414)

All trademarks, service marks and trade names referenced in this material are the property of their respective owners.